The global bio-based adhesives market is expected to grow at a CAGR of 4.85% until 2027, according to a new report from ResearchAndMarkets. The global industry is expected to witness an absolute growth of 32.85% during the forecast period. Factors like evolving emission regulation across the globe, rapid industrialization across emerging economies, and the stringent regulation to limit the use of formaldehyde material in wood panels are driving the market.

Globally, the demand for bio-based adhesives are due to several reasons, including environmental concerns to reducing carbon footprints, a reduced dependency on fossil fuels, and the existence of strong regulatory bodies.

Bio-based adhesives such as proteins, lignin, natural resin, vegetable oils, and starch are vital components in formulating bio-based adhesive products. These adhesives are playing an increasingly vital role in preserving the environment by preventing the release of harmful chemicals. They’re also meeting ever-increasingly stringent government standards, related to carbon emissions while maintaining high performance.

Regulatory bodies such as the United States Green Building Council, California Air Resources Board (CARB), and European Union have set the regulations and standards such as REACH, CLP, and the circular economy initiative that mandate the use of green adhesive across various applications. Such regulations can be broadly classified into product type and application segments.

The established bio-based adhesives markets of North America and Europe are expected to witness high demand for bio-based adhesive products during the forecast period due to the strong regulatory landscape for the bio-based product and unprecedented growth across the packaged food, pharmaceutical, furniture, and residential and non-residential construction industries due to the surge in private investment.

Market trends

- Escalating demands from the packaging industry. Increasing purchasing power, an increasing pace of urbanization, rapid growth of the e-commerce industry, and expanding population are driving the packaging industry market, globally. This growth is expected to generate significant demand for bio-based adhesives products because it offers strong bonds and adhesion for manufacturing corrugated packaging, paperboard, and case and carton. Such factors create a positive impact on the bio-based adhesives market. Furthermore, bio-based adhesives also offer transparent packaging while assisting manufacturers in meeting operational budgets and enabling manufacturers to meet the rising demand for antiviral and antibacterial packaging.

- Rising sustainability concerns. Sustainability has become a significant concern for the consumer and industry. In the past, adhesives were formulated from fossil fuel-based chemicals such as urea-formaldehyde, Methylene diphenyl diisocyanate, and phenol. However, with increasing demand for safer and greener adhesives, companies are developing environment-friendly production processes and using renewable resources to fulfill the increasing demand for bio-based alternatives that promotes sustainability. Production of adhesives from renewable feedstock is helping various industries in reducing their carbon footprint. Therefore, industries such as paper & packaging, OEMs, construction, and woodworking have decided to implement strategies promoting sustainable development so that companies can maximize profits while adding value to society.

Market restrains

- Stiff competition from low VOC adhesives. The major challenge faced in the global bio-based adhesives market is the high dominance of low volatile organic compounds (VOC) adhesives. Low VOC adhesives are user-friendly as a bio-based because during formulation, no safety measures are required. These adhesives are environmentally friendly and do not risk human or aquatic life by releasing toxic or odorous fumes. In addition, stringent environmental regulation mandated by the U.S. Environmental Protection Association (USEPA), Leadership in Energy and Environmental Design (LEED), and the European standards of EN 16785-1 verifies bio-based content of the product are also driving the demand for low VOC products.

Feedstock considerations

Sugar is one of the essential components in the global bio-based adhesives market under the feedstock segment. It generally includes starch, cane, and beet. The segment is expected to hold the largest global market share and will reach U.S. $3.87 billion by 2027.

The global glycerol bio-based adhesives market was valued at $1,520.71 million in 2021 and emerged as the second-largest segment in the market, with a revenue share of 28.83%. Glycerol is the most important feedstock used in the adhesive industry — not only as a binding agent but also as a sustainability. Vegetable oils and saponification of oils and fats are used to produce glycerol. It’s a versatile compound due to its chemical properties and environmental benefits, making it effective in synthesizing polymers and adhesive products.

Segmentation by feedstock

- Sugar

- Glycerol

- Oil & Fats

- Biogas

- Others

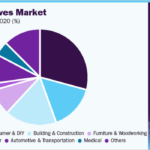

Applications

Based on application, the global bio-based adhesives market is divided into six segments: paper & packaging, construction, woodworking, personal care, medical equipment, and others.

Paper & packaging held the largest share in the industry in 2021, and it is also expected to lead the market during the forecast period. This is primarily due to the increasing demand for ready-to-eat food, microwave-ready meals, and packaging for on-the-go consumption that consumes bio-based adhesives for bonding pouches, sachets, bags, and corrugated board due to their natural composition that adheres well, when applied on high-surface tension substrates and permeable surfaces.

Segmentation by application

- Paper & Packaging

- Construction

- Woodworking

- Personal Care

- Medical Equipment

- Others

Geographical analysis

North America emerged as the leading consumer of bio-based adhesives and accounted for a revenue share of 41% of the global bio-based adhesives market. The region was led by the U.S. and Canada, where the penetration of adhesive products is high, and the market revenue has been increasing steadily.

Factors like the rise in focus on sustainability to reduce carbon footprint, the stringent regulations to restrict the use of formaldehyde in wood panels, and the surge in the growth of the packaged food, medicines, and construction output drives the demand for bio-based adhesives product in North America.

Europe was the second-largest bio-based adhesives market, with a 27% revenue share in 2021. The presence of top-notch manufacturers such as Jowat (Germany), Intercol Industrial Adhesive (Netherland), Henkel (Germany), and Beardow Adams (UK) contributes to the significant growth of the bio-based adhesive market as these companies make use of renewable sources for formulating adhesive.

Competitive landscape

The global bio-based adhesives market is nascent and expected to accelerate during the forecast period. The market is characterized by a few large and small players such as Jowat (Germany), Bostik (Arkema) (France), TOYOCHEM (Tokyo), and Conagen (U.S.), among others.

The changing market scenario with an emphasis on reducing carbon footprint and promoting sustainability affects vendors as customers expect continual innovations and upgrades. In response to it, several vendors in the market are working closely with the end-use industry players to understand customer expectations while keeping in mind the sustainability aspect.

Hence, the bio-based adhesives market will offer significant growth opportunities to the existing and new players.

Key vendors

- Bostik

- Beardow Adams

- Henkel

- Jowat

Tell Us What You Think!